When 29-year-old Perth electrician Jake Morrison checked his July payslip, he noticed a slight bump in his employer’s super contribution. It wasn’t dramatic, but it marked a milestone: the Super Guarantee had officially reached 12%.

“It doesn’t feel like much now,” Jake says, “but I’ve been told it makes a big difference long term.”

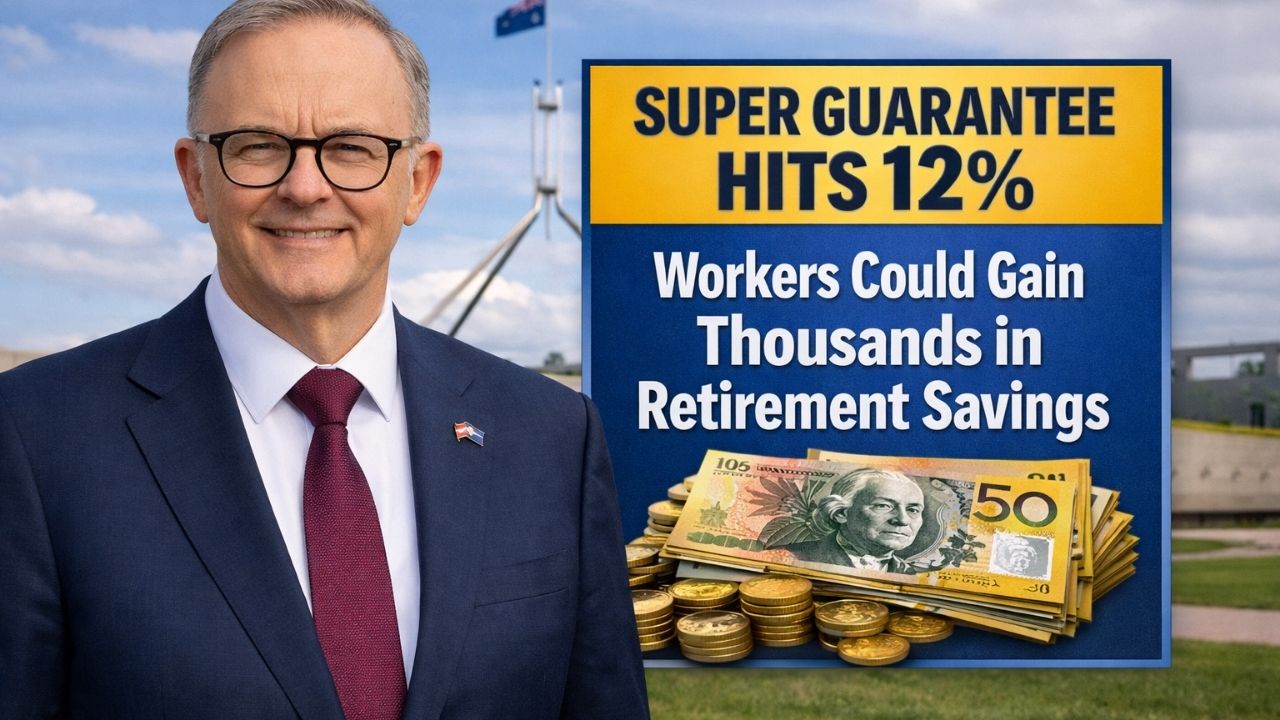

From 1 July 2026, Australia’s compulsory superannuation contribution rate increased to 12%, completing a multi-year phase-in. While the jump from 11.5% to 12% may seem small, financial experts say it could translate into thousands — even tens of thousands — of extra retirement savings over time.

Here’s why 2026 is a turning point for Australian workers.

What the 12% Super Guarantee Means

The Super Guarantee (SG) requires employers to contribute a percentage of an employee’s ordinary time earnings into their super fund.

From July 2026:

- The SG rate is 12%.

- The increase is permanent.

- It applies to most full-time, part-time and eligible casual workers.

- Employers must comply or face penalties.

A fictionalised Treasury spokesperson said, “The 12% rate strengthens long-term retirement outcomes for Australian workers.”

This marks the highest compulsory rate in Australia’s history.

How Much Extra Could You Gain?

While the 0.5% increase may appear modest, compounding over decades magnifies its impact.

Example:

If you earn $90,000 per year:

- At 11.5% → $10,350 annually in super.

- At 12% → $10,800 annually.

- Difference → $450 per year.

Over 30 years, assuming steady employment and average investment returns, that additional contribution could grow significantly due to compound interest.

For younger workers, the long time horizon makes 2026 especially important.

Financial adviser (fictionalised) Emma Richards explains, “Time is the most powerful factor in super growth.”

Why 2026 Is a Strategic Year

Several retirement trends make 2026 pivotal:

- The 12% rate is now locked in.

- Retirement savings targets are rising.

- Australians are living longer.

- Super balances are increasingly central to retirement income.

- Market volatility has highlighted long-term investing discipline.

Workers who review their super strategy now can maximise the benefits of the higher contribution rate.

Retirement Targets Are Climbing

In 2026, estimates suggest:

- Singles may need over $600,000 for a comfortable retirement.

- Couples may require around $730,000 combined.

Longer life expectancy and elevated living costs mean super balances must stretch further.

The 12% contribution rate improves the likelihood of reaching these benchmarks — especially for workers in their 20s, 30s and 40s.

Who Benefits Most?

The biggest long-term beneficiaries include:

- Younger workers with decades until retirement.

- Employees with consistent income growth.

- Individuals who avoid withdrawing super early.

- Workers who consolidate multiple super accounts.

- Those who make voluntary contributions.

Jake says, “I’ve got 35 years ahead of me — that’s when it counts.”

For workers nearing retirement, the impact is smaller but still meaningful.

Does 12% Affect Take-Home Pay?

In most cases:

- Super contributions are paid on top of your wage.

- Your take-home pay remains unchanged.

However, if you’re on a “total remuneration package” that includes super, the increase may slightly affect net pay.

Workers should review employment contracts to confirm how super is structured.

Voluntary Contributions Still Matter

While 12% is an improvement, experts say it may not guarantee a comfortable retirement on its own.

Workers can also consider:

- Salary sacrifice arrangements.

- After-tax voluntary contributions.

- Government co-contribution schemes (for eligible low-income earners).

- Spouse contributions.

Even an additional $20–$50 per week can significantly boost long-term savings.

Economist (fictionalised) Dr. Laura Bennett notes, “Compulsory super builds the foundation — voluntary contributions accelerate growth.”

Market Volatility and Long-Term Perspective

Super funds invest across:

- Shares.

- Bonds.

- Property.

- Infrastructure.

Short-term market fluctuations are normal, but super is designed for long-term growth.

Regular contributions — especially at 12% — smooth market cycles over time.

Workers who stay invested during downturns historically benefit more over decades.

Real Stories Behind the Change

Jake plans to keep his contributions at the compulsory rate for now.

“I might add extra once my mortgage is smaller.”

Meanwhile, 45-year-old marketing manager Sarah has begun salary sacrificing an extra $100 per fortnight.

“With 12% already going in, I want to build momentum.”

Different strategies suit different life stages.

What Workers Should Do in 2026

To maximise the 12% milestone:

- Check your payslip to confirm correct contributions.

- Review your super fund’s fees and performance.

- Consolidate multiple accounts.

- Update beneficiary nominations.

- Consider voluntary contributions if affordable.

- Review insurance inside super.

Small proactive steps now can compound significantly over time.

Q&A: Super Guarantee 12% in 2026

1. When did the 12% rate begin?

1 July 2026.

2. Does this increase my take-home pay?

Usually no — contributions are separate.

3. Is 12% enough for retirement?

It improves outcomes but may not guarantee comfort alone.

4. Who is covered?

Most employees, including part-time and many casual workers.

5. Will the rate increase further?

There are no scheduled increases beyond 12%.

6. Should I make extra contributions?

If affordable, it can significantly boost long-term savings.

7. Does this affect self-employed workers?

They must contribute voluntarily.

8. Can I check if my employer is compliant?

Yes, through your super fund statements.

9. Why is 2026 important?

It marks the completion of the phased SG increase.

10. What if I’m close to retirement?

Even a few years at 12% can help strengthen your balance.

In 2026, the Super Guarantee reaching 12% represents a major structural milestone for Australia’s retirement system.

While the increase may seem small on each payslip, its long-term impact could mean thousands more in retirement savings — particularly for younger workers with decades of compounding ahead.

For Australians like Jake, 2026 isn’t just another financial year — it’s the year retirement savings quietly became stronger.

Leave a Comment