When 69-year-old former mechanic Trevor Dawson retired three years ago, he believed his superannuation and Age Pension would be enough. But by early 2026, rising rent, groceries, insurance, and power bills pushed him back into the workforce part-time.

“I didn’t expect to be job hunting at my age,” Trevor says. “But I needed the extra income.”

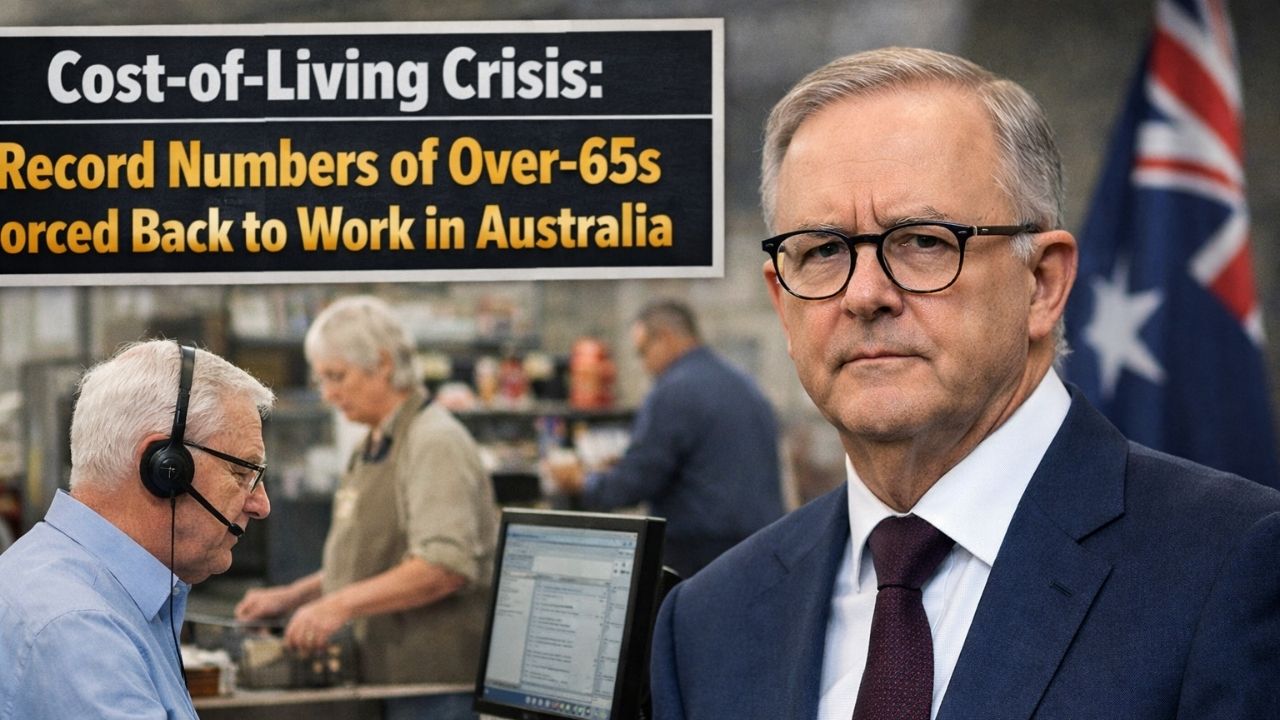

Across Australia, record numbers of people aged over 65 are returning to work or delaying retirement due to mounting cost-of-living pressures. What was once considered a stable retirement phase is increasingly becoming a period of financial adjustment.

Here’s what’s driving the trend — and what it means for seniors in 2026.

Over-65 Workforce Participation Hits New High

Labour force data shows a steady increase in Australians aged 65 and older remaining in employment.

Key drivers include:

- Rising housing costs.

- Higher energy and grocery prices.

- Insufficient superannuation balances.

- Longer life expectancy.

- Increased part-time and flexible job opportunities.

Many seniors are not returning to full-time work but taking on:

- Casual retail shifts.

- Consultancy roles.

- Delivery services.

- Community-based positions.

- Part-time administration jobs.

Economist (fictionalised) Dr. Karen Holt says, “Retirement is no longer a fixed endpoint. For many, it’s a transition into reduced but ongoing work.”

Why Super Isn’t Stretching Far Enough

Although the Superannuation Guarantee has now reached 12%, many current retirees contributed under much lower rates during their careers.

Challenges include:

- Career breaks (especially among women).

- Part-time employment histories.

- Market volatility affecting investment returns.

- Early withdrawals during past financial stress periods.

With retirement often lasting 20–30 years, savings can deplete faster than expected.

For singles, retirement experts estimate that over $600,000 may be needed for a comfortable retirement — a target many fall short of.

Rising Costs Driving the Return to Work

Cost-of-living pressures in 2026 include:

- Higher rental prices, particularly in metropolitan areas.

- Insurance premium increases.

- Electricity and gas price volatility.

- Medical and health-related expenses.

- General inflation affecting groceries and essentials.

For renters, the situation is especially challenging.

Trevor rents in Brisbane and says, “Rent went up twice in two years. That alone changed everything.”

Pension Indexation Isn’t Always Enough

The Age Pension is indexed twice yearly to inflation and wages. While increases provide relief, they may not fully offset sharp spikes in specific expenses.

For full-rate single pensioners:

- Payments exceed $1,100 per fortnight.

- Supplements are included.

- Rent Assistance may apply.

But for part pensioners, income and asset tests can limit payments.

Policy analyst (fictionalised) Martin Shaw notes, “Indexation helps, but when expenses rise unevenly — especially housing — seniors feel squeezed.”

Real Stories Behind the Statistics

Margaret, 72, works two mornings a week at a local library.

“I enjoy it, but honestly, I wouldn’t be working if prices hadn’t gone up so much.”

Meanwhile, 67-year-old David postponed retirement entirely.

“I planned to stop at 67. Now I’m aiming for 70. Every extra year boosts my super.”

These examples show that motivations vary — but financial necessity is increasingly common.

The Work Bonus Incentive

To support older workers, Centrelink’s Work Bonus allows Age Pension recipients to earn employment income without immediate pension reductions.

Under current settings:

- A portion of employment income is excluded from the income test.

- Unused credits can accumulate.

- It encourages flexible, part-time work.

This scheme has helped many seniors balance pension payments with paid work.

Health and Inequality Concerns

While some seniors choose to work, others feel compelled.

Physical limitations can restrict job options, particularly for those from manual labour backgrounds.

Inequality becomes visible when:

- Professionals with higher super balances retire comfortably.

- Lower-income retirees must continue working to survive.

Community advocate (fictionalised) Angela Brooks says, “Not everyone can physically continue working into their late 60s or 70s.”

Comparison: Retirement Then vs Now

| Factor | 20 Years Ago | 2026 Reality |

|---|---|---|

| Typical Retirement Age | 65 | 67+ and rising participation |

| Super Contribution Rate | Lower | 12% |

| Workforce Participation 65+ | Lower | Record high |

| Cost-of-Living Pressure | Moderate | Elevated |

The expectation of retiring fully at 65 has shifted significantly.

Psychological Impact

Returning to work can:

- Improve social engagement.

- Boost mental stimulation.

- Reduce isolation.

However, financial stress remains the primary motivator for many.

Trevor admits, “It’s good to stay busy, but I’d rather be fishing.”

What Seniors Can Do in 2026

If you’re facing similar pressures:

- Review your pension eligibility.

- Ensure income reporting is accurate.

- Explore the Work Bonus.

- Consider downsizing options.

- Seek financial advice about super drawdown strategies.

- Check eligibility for concessions and supplements.

Even modest adjustments can ease financial strain.

Is This Trend Likely to Continue?

Experts suggest workforce participation among over-65s may remain elevated due to:

- Longer life expectancy.

- Improved health in later years.

- Ongoing economic uncertainty.

- Superannuation gaps among current retirees.

Younger generations benefiting from 12% super contributions may face different outcomes decades from now.

Q&A: Seniors Returning to Work 2026

1. Are more over-65s working in 2026?

Yes, participation rates are at record levels.

2. Why are seniors going back to work?

Rising living costs and insufficient savings.

3. Can I work while receiving the Age Pension?

Yes, subject to income test rules.

4. What is the Work Bonus?

A scheme allowing pensioners to earn employment income with reduced impact on payments.

5. Does working reduce my pension?

It may, depending on earnings.

6. Is retirement age increasing?

The Age Pension age remains 67.

7. Are renters more affected?

Yes, housing costs are a major driver.

8. Does superannuation affect pension eligibility?

Yes, if you are drawing income from it.

9. Is this trend permanent?

It may continue if economic pressures persist.

10. Are there health risks in working longer?

It depends on the individual and job type.

11. Can I partially retire?

Yes, phased retirement is common.

12. Do women face greater challenges?

Often yes, due to lower lifetime super balances.

13. Is pension indexation enough?

It helps but may not fully offset rising costs.

14. What industries hire older workers?

Retail, community services, consulting, and administration.

15. Is returning to work a failure?

No — many seniors balance work and retirement strategically.

For many Australians over 65, retirement in 2026 looks different from past generations.

While some work by choice, record numbers are doing so out of necessity. As living costs rise and savings stretch thin, the line between retirement and employment continues to blur.

In today’s economic climate, financial resilience often means adapting — even in later life.

Leave a Comment